Bro, Where Are My Transformers?

Venture Capital has quickly become the ‘who invests in AI company X, Y, Z, first’ race. Besides quick returns, there is more to this story. Here’s the breakdown.

Sup! 👋

It was about time to write about another VC-related topic.

Don’t worry, I will have some unique X-posts and profound takes in this one, but it will mainly be a numbers piece.

Something like 80% of all VC cheques in the last two years went into AI businesses or startups with heavy AI exposure.

And we’re at a point where it’s complete madness!

There are so many things to elaborate and explain here, so let’s not waste any time and get stuck in right away!

PS: If you enjoy this newsletter and believe your friends or family would too, a recommendation would be greatly appreciated!

In Q1 2026, global venture capital hit $300 billion.

Eighty percent went to AI. Sixty-five percent went to four companies!

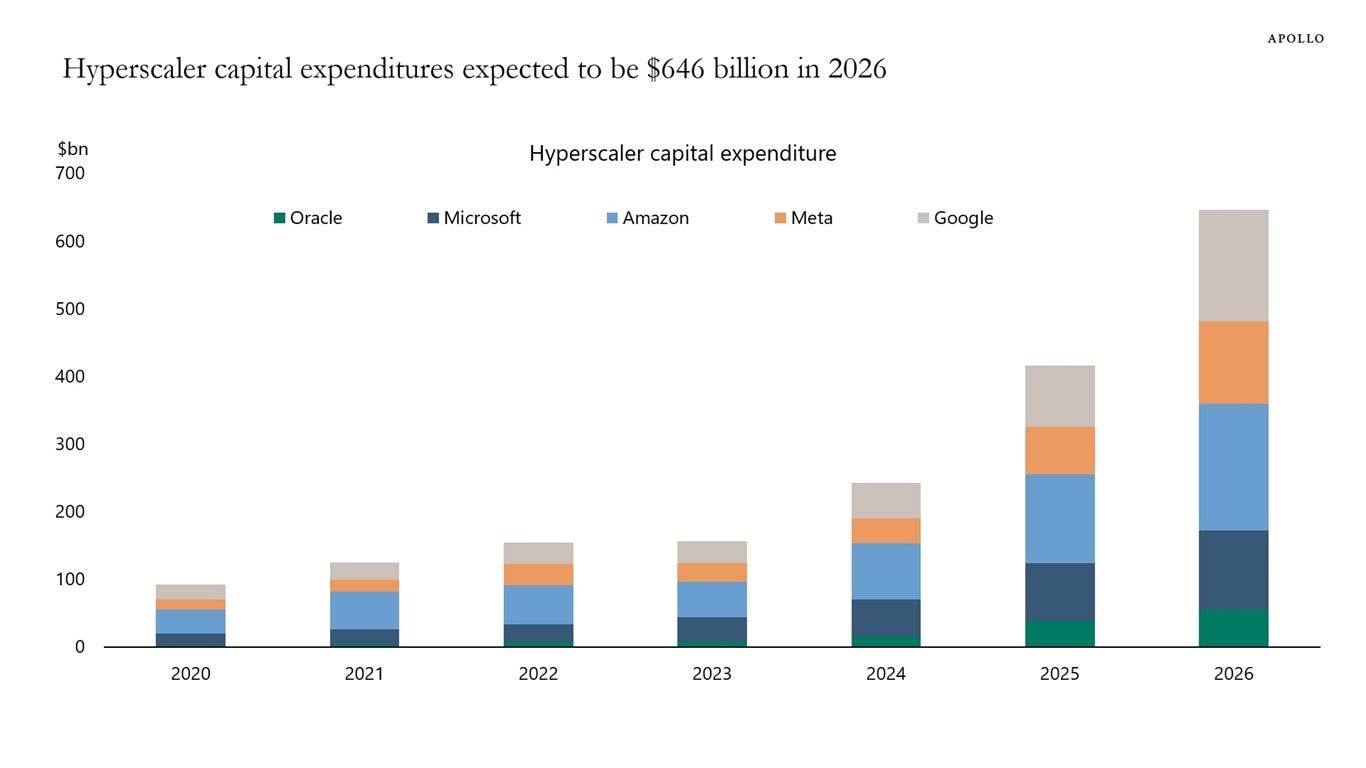

In the same quarter, hyperscalers committed another $650 billion to building the data centers that will house all those promises.

Out of 12 gigawatts of US data center capacity planned for 2026, only 5 are actually being built.

Capital outran the grid.

The rest is delayed, canceled, or waiting on transformers that take up to five years to ship.

The bottleneck on AI in 2026 isn’t models or chips. It’s electrical equipment, most of it sourced from China.

The bubble pops on power, not on valuations.

So bro, where are the transformers?

Well, the simple answer is: they went to four companies, and there isn’t much we can do right now.

The more complex answer is the following.

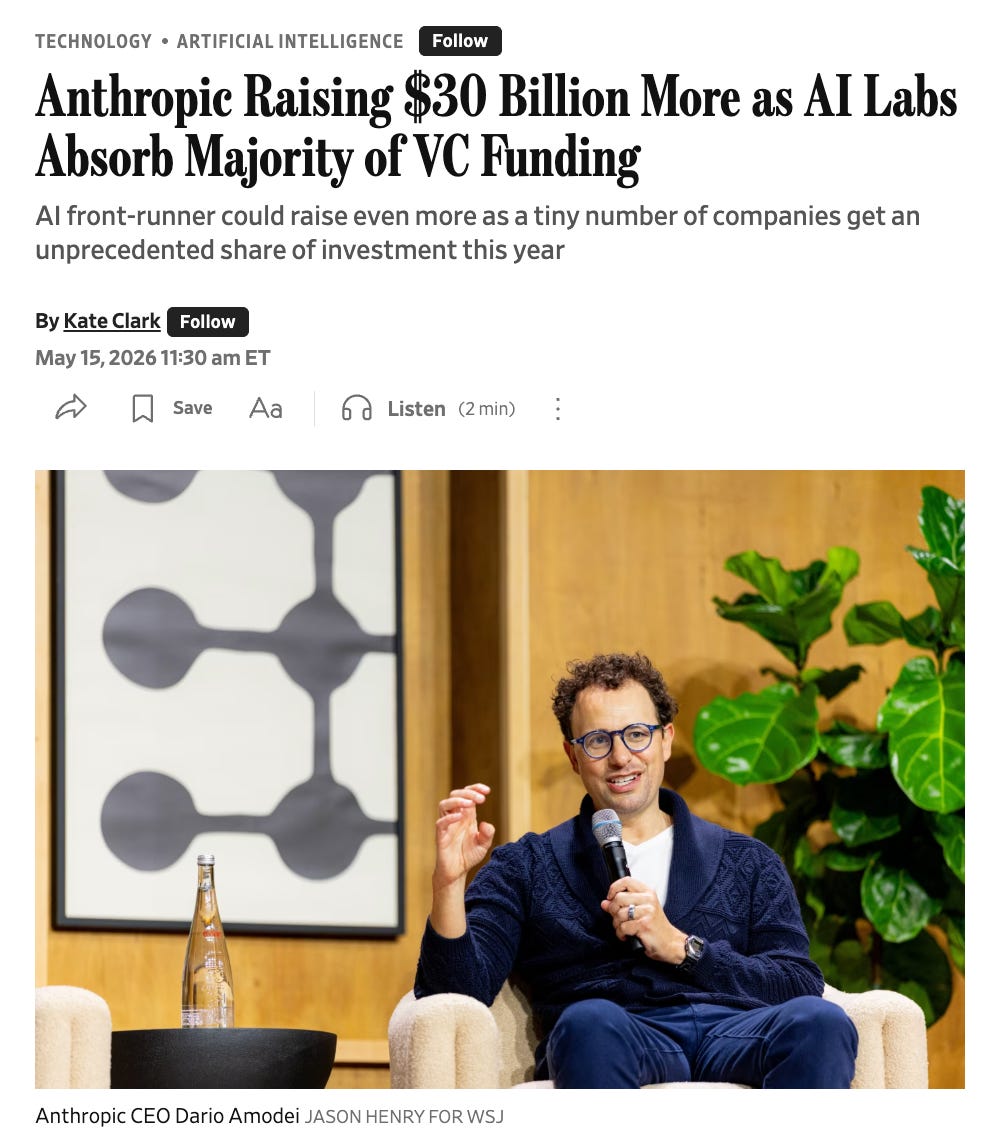

OpenAI raised $122 billion. Anthropic raised $30 billion. xAI raised $20 billion. Waymo raised $16 billion.

Together, those four deals ate 65% of all global venture funding for the quarter.

Source: Wall Street Journal

That math should bother you, regardless of what you think about AI.

A year ago, AI captured roughly half of global venture funding. Now it’s eighty percent.

Q1 2026 alone exceeded all of 2025 combined for AI investment. The remaining 20% that went to non-AI startups.

LPs allocating to “venture” in 2026 aren’t buying diversification. They’re buying a concentrated bet on four operating companies, dressed up in a venture wrapper.

Talk to any solo GP raising funds right now. The first question from LPs isn’t about portfolio construction or thesis. It’s about AI exposure.

As if AI exposure were a primitive that exists separately from the four companies that have already absorbed it all.

The honest version of that conversation: every fund without allocations to OpenAI, Anthropic, xAI, or Waymo is implicitly betting against the median LP’s preferred trade.

That’s a brave position to underwrite, and also the only one with any chance of generating differentiated returns.

The result is a venture market with two tiers. The top tier writes massive checks into a handful of late-stage AI deals at valuations that may or may not survive a deployment timeline they don’t control.

The bottom tier hunts for AI-adjacent picks, deep tech, and vertical SaaS bets that LPs increasingly view as consolation prizes.

There’s no middle anymore, and the grid says no.

Source: Bloomberg

Sightline Climate, the market intelligence firm, tracks roughly 12 GW of US data center capacity scheduled to come online this year.

Bloomberg reported in April that close to half of those projects are delayed or canceled.

Can you imagine that?!

Out of about 140 planned facilities, only a third are actively under construction.

The reason isn’t capital, rather it’s transformers.

Lead times for high-power transformers ran 24 to 30 months before 2020.

Today, they can stretch to five years. AI deployment cycles run under 18 months. The math doesn’t work.

Specifics make the abstract real. Micron’s reported $24 billion Singapore fab is going to need hundreds of transformers, more than the annual output of any single manufacturer in the world.

Hyperscaler projects across Texas, Virginia, and Arizona are running into operator disputes, environmental opposition, and supply chain delays that wouldn’t have stopped a project in 2019.

Source: YouTube

The 7-gigawatt gap isn’t one big problem; there are hundreds of smaller problems, all happening at once.

Developers are scrambling for alternatives. Canada, Mexico, and South Korea have become major transformer suppliers to the US AI build-out.

Imports of Chinese high-power transformers, despite tariffs and national security concerns, jumped from fewer than 1,500 units in 2022 to more than 8,000 through October 2025.

China supplies more than 60% of US battery imports and roughly 20% of certain transformer and switchgear categories.

The country the US has spent a decade trying to reshore manufacturing away from is now the one keeping the AI build-out alive.

Most AI bubbles take focus on valuations. Wrong stress point!

The valuations might survive a sentiment correction. They won’t survive a deployment timeline that physically cannot be delivered.

Source: Apollo Academy

If hyperscalers spend $650 billion in 2026 to build capacity that arrives 18 months late, the inference compute promised in every enterprise pitch deck doesn’t exist on schedule.

Customers don’t churn because they don’t have alternatives. They also don’t expand the way the projections require.

The unmet demand becomes a 2027 markdown story.

Worth flagging here: this is also why OpenAI’s DeployCo arrangement, the $10 billion structure where it’s promising private equity firms a 17.5% guaranteed return for distribution rights inside their portfolios, looks shakier the more you stare at it.

Mandating AI deployment across 1,200 portfolio companies sounds great until you realize the inference compute to serve those rollouts may not be online when the contracts say it should be.

I will tackle DeployCo in an upcoming piece, so watch out for that.

But still, the grid is the binding constraint. Capital can’t fix it on the timeline. LPs are underwriting.

However, this analysis, if you want to call it that, is very one-sided and mainly focused on the U.S.

Source: Gulf News

I’m writing this from Dubai, in an undercooled room, but with a strong focus on how other regions around the world are doing this differently.

The dollar venture pool is locked into four labs that all need US power and US grid permits to deliver what they’ve sold.

Meanwhile, sovereign capital in the UAE, Saudi Arabia, and Singapore is sitting on actual energy infrastructure, faster permitting, and a willingness to fund grid build-outs directly.

The UAE doesn’t have a five-year transformer queue; at least I couldn’t find any official data or resources on it.

G42 is already operating a gigawatt-scale infrastructure in Abu Dhabi, with backing from Microsoft and the local sovereign wealth machinery.

Saudi Arabia’s PIF launched HUMAIN as the kingdom’s national AI champion, with capital deployment speeds that don’t run through any Western allocation committee.

Source: YouTube

Singapore is quietly rebuilding itself as a regional data center hub with regulatory clarity that Washington has spent a decade failing to deliver.

These projects and initiatives aren’t moonshot bets. They’re operating projects with existing power, existing permits, and access to capital that doesn’t ask whether AI is in a bubble.

Nobody is suggesting every AI workload should move to the Middle East.

The question is why $242 billion of Q1 capital ignored the geographies where the deployment surface is actually being built.

The answer is partly inertia, partly LP comfort with US tech, and partly currency.

None of those reasons holds forever.

The next leg of the AI cycle belongs to the regions that figure out how to put compute where the power already is.

OK, enough numbers, companies, or even geography talk.

As I showed, the world of VC investing into AI, and the lack of transformers, is a story with many backroom deals.

But there was more going on this week as well, or some things I find interesting. Some of it is funny, some is a long read, and other things are just flat out crazy.

Here are the Tabs Worth Opening:

This Danish newspaper still has more paper readers than online subscribers: Weekendavisen newspaper is one of these rare stars in the media industry. The paper is run by Martin Krasnik, and in this Monocle interview, he showed that they are still selling more physical papers than online subscriptions.

A guy recovers his Bitcoin wallet with Claude: This was making the rounds on X. A Bitcoiner forgot the password to one of his BTC wallets from 2013. Thanks to Claude and some reverse engineering, he recovered its password. Make no mistakes here, Claude didn’t ‘hack’ the wallet. It merely found out what password he most likely had.

You can now take OpenAI’s Codex everywhere with you: Many people, especially the OpenClaw community, are using OpenAI’s Codex as their Claude Code alternative. And this week, the company announced that you can now connect your Codex instances and account to your mobile ChatGPT app.

Google is gearing up for its developer conference: Alex Heath from Sources reported that the company will soon release a new version of Gemini. They also released Googlebook, the comeback of their famous Pixelbook, now with dedicated AI features.

The Senate Banking Committee voted in favor of the Clarity Act: This news might only be interesting to crypto nerds. Still, the Senate Banking Committee just greenlit the approval for the Clarity Act. This regulation would ensure the full integration of crypto assets into the banking system. Let’s see if the vote passes in the Senate. They need at least 60 in favor.

And that’s a wrap for the eleventh full issue of Internet Native Capital.

It was a longer one than expected, with many numbers, scenarios, and potential future outcomes.

I hope you liked it, and I answered the question of why the transformers are missing and why VCs are only investing in AI at the moment.

I’ll now head out for a well-deserved walk around the block and a nice iced coffee.

See ya!

The bubble doesn't pop on valuations but on power and the grid says no.

AI money is massively concentrated in a few players, and the real constraint is physical infrastructure like power and transformers that can’t scale fast enough