Deployco, AKA OpenAI’s Master Lease - Genius or the End of the Beginning?

Sam Altman is busy in a courtroom with Elon Musk currently, and soon maybe with Apple Inc. To keep making money, he convinced PE firms to invest in his vision. More on that here.

Sup! 👋

Sam Altman has officially entered his villain era.

Doesn’t matter if you read the New Yorker, watch an interview, or scroll through any Substack deep-dive worth its salt.

People don’t trust Sam’s word anymore.

Some of that has to do with all the broken promises along the way, and some of it is the AI hype cycle finally catching up with the guys selling the dream.

Now picture this: OpenAI rolls out a shiny new business structure in which it pays private equity firms a 17.5% annual yield for exposure to roughly 1,200 portfolio companies.

Yes, you read that correctly. A guaranteed return. From an AI company. To Blackstone and friends.

The skepticism online has been off the charts, and the newly formed DeployCo is getting cooked daily on X.

Today, I’m breaking it all down, walking you through how the structure actually works, and showing why this is, in my book, AI’s WeWork moment.

PS: If you enjoy this newsletter and believe your friends or family would too, a recommendation would be greatly appreciated!

Adam Neumann would be proud.

And I’m not talking about a big ass party in the middle of somewhere, I’m talking about OpenAI’s latest deal-making.

Two weeks ago, OpenAI disclosed The Deployment Company, a $10 billion vehicle backed by TPG, Brookfield, Advent, Bain, and 15 others.

Sam Altman’s company is paying the private equity consortium a guaranteed 17.5% annual return for five years in exchange for one thing: access to the operating businesses within their portfolios.

Roughly 1,200 companies, with mandated AI distribution, knowledge from industry experts, and financed in advance.

Source: OpenAI

DeployCo is a master lease in everything but name. The bet is just that the underlying works this time.

And if this works, there is a lot of money at stake!

PE firms invested $4 billion over the five-year window. OpenAI put in $1.5 billion of its own money: $500 million upfront, with an option to add another $1 billion later.

The vehicle is Delaware-domiciled, run by Brad Lightcap (until recently OpenAI’s COO), and structured so that OpenAI keeps strategic control through super-voting shares.

The PE backers get yield. OpenAI gets distribution.

The mechanism is borrowed from Palantir. So-called “forward-deployed engineers” embed inside client companies, customizing AI integrations on-site.

It’s expensive and high-touch. It also converts what would otherwise be six-month enterprise sales cycles into mandates.

When a PE firm owns the cap table of an operating company, “Should we evaluate AI tools?” stops being a real question.

It becomes a procurement formality, kinda like the WeWork Trick, updated.

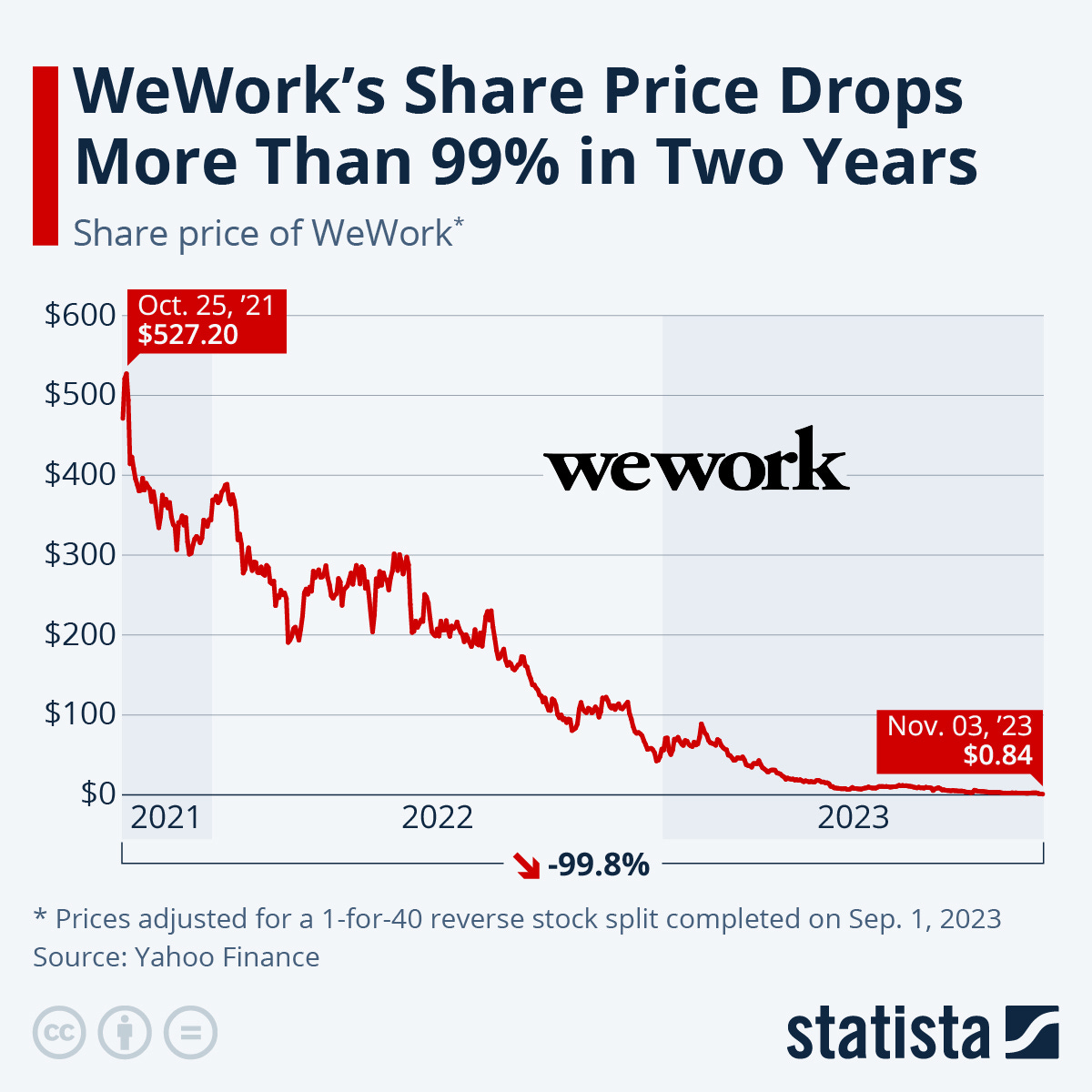

In its peak years, WeWork signed long-dated master leases with landlords and property SPVs. The company was on the hook for the rent regardless of whether tenants showed up.

The guarantees were backstopped by venture capital and a thesis about future demand for flexible office space.

When occupancy didn’t grow the way the model required, the guarantees became the problem.

Source: Statista

WeWork’s master lease portfolio peaked at $47 billion in committed payments. The IPO failed in September 2019 once underwriters got serious about modeling those obligations.

SoftBank had to write down its position by tens of billions to keep the company alive. The 2023 Chapter 11 filing was, in functional terms, a renegotiation of the master leases that should have happened four years earlier.

The lesson wasn’t that WeWork was a bad business. The lesson was that operators who guarantee fixed payments based on demand projections are running an insurance business, whether they call it that or not.

DeployCo is the same financial engineering, with different counterparties. OpenAI is the operator. PE firms are the financial counterparties.

The 17.5% guarantee is functionally a fixed lease payment. The thesis is on enterprise AI adoption within 1,200 portfolio companies.

The structural similarity isn’t a prediction about how it ends. WeWork was selling a commodity (office space) in a saturated market.

OpenAI is selling frontier AI into a market that’s nowhere near saturation. The underlying might genuinely work this time.

But the financial engineering is identical, and it’s exactly that modeling we should take a look at today.

17.5% yield, that’s the key number you need to focus on. Why? Well, standard enterprise software companies don’t guarantee returns to anyone.

The product sells itself. Customers churn or expand based on whether it works. The whole point of having a great enterprise tool is that the unit economics speak for themselves.

OpenAI guaranteeing 17.5% to PE firms is, structurally, an admission that the enterprise sales motion isn’t getting them where they need to be on the timeline they need.

Source: Blackstone

Anthropic is running a parallel deal with Blackstone, Hellman & Friedman, and Permira at roughly $1 billion.

The difference matters: Anthropic isn’t offering a guaranteed return. It’s selling common equity to its PE partners.

The implicit message is that Anthropic doesn’t think its product needs a yield sweetener to get distribution. Two different bets about the state of enterprise AI sales.

While these deals are impressive and some of the financial analysts will love the models they spun up, there is one group that’s being left out of this discussion: local communities.

To scale at this size, you need data centers. Currently, there is a bidding war over land and over where to build out these infrastructure projects.

Local communities are pushing back hard, not only over uncertainty about whether this will mean cost-cutting for local builders, but also over environmental concerns.

As it’s often the case with such financial expansion models, the little man is being left out of the discussion, and I think we will see a future where a lot of ‘anti-AI’ movements will emerge.

The DeployCo structure has a second-order effect that most coverage hasn’t unpacked.

When PE firms commit to deploying OpenAI’s tools across their portfolios in exchange for guaranteed yield, they’re not just buying distribution rights. They’re effectively committing not to deploy competing AI tools at the same scale.

That’s bad news for Anthropic. Worse news for the second tier of AI companies, including Mistral, Cohere, and the open-weights ecosystem.

Worst news for whichever startup thought it could compete in vertical AI by selling into PE-owned operating businesses.

If your enterprise AI startup depended on PE-owned operating companies as your beachhead market, that beachhead just got rented for five years.

OpenAI didn’t just buy distribution, rather it bought distribution scarcity.

But for some reason, the math isn’t mathing…

A 17.5% annual return on $4 billion of preferred equity comes to about $700 million per year.

Across the five-year horizon, that’s roughly $3.5 billion in guaranteed distributions, plus principal protection.

OpenAI is projecting a $14 billion loss for 2026, even at roughly $30 billion in annualized revenue.

The DeployCo math only works if enterprise AI adoption across 1,200 portfolio companies generates more than $700 million per year in net contribution after accounting for the cost of forward-deployed engineers, implementation overhead, and the ongoing infrastructure required to serve those workloads.

It also requires that the inference compute to serve all that adoption actually exists on schedule.

Source: Polymarket

This connects to the previous piece. Of the 12 GW of US data center capacity planned for 2026, only 5 are under construction.

The grid is the binding constraint on every promise being made in 2026, including this one.

Which brings me to my point of the story.

Tech companies don’t issue fixed-yield paper. Insurance companies do. What OpenAI did with DeployCo is convert future enterprise AI revenue into present-day fixed-income obligations.

Call it growth equity if you want. It doesn’t behave like growth equity. It behaves like an annuity, dressed up in tech clothing.

The problem with operating companies issuing structured products isn’t the structure itself, rather it’s the distortion.

Capital allocation decisions get pulled toward whatever protects the yield commitment. Risk doesn’t sit well with the people best placed to manage it.

In a world where enterprise AI adoption hits the projections, this is brilliant.

Distribution gets locked in. Revenue gets pulled forward. Competitors get shut out of the same PE portfolios.

But, in a world where it doesn’t, OpenAI just sold its growth optionality at 17.5% per year for the next five years, all while fulfilling previous commitments.

That’s not the trade I’d have made. But I’m not the one trying to compete with Anthropic on enterprise distribution before an IPO.

The whole DeployCo story is either going to be the best thing Sam Altman has ever done, or the beginning of the end for the ChatGPT makers.

Either way, we have to wait and see what will emerge in the coming months.

But that wasn’t the whole story this week. As a matter of fact, this was a jam-packed week with a lot of side stories.

I tried to recap all of them in this segment and will for sure cover many of them in the next couple of write-ups.

Here are the Tabs Worth Opening:

Google caught up with the AI mega labs: This week was Google I/O week. And they announced many new Gemini features. From Spark, the OpenClaw answer for normies, to new Gemini models, even more confusion with a new pricing plan, and new AI hardware. Expect a full write-up soon!

SpaceX’s IPO is on, and Elon Musk needs to bet big: SpaceX needs to be a big hit! Not only because he attached the future of X and its AI lab to it, but also because he lost to Sam Altman in court earlier this week. The IPO is scheduled as early as next month, with a potential listing soon!

Anthropic and OpenAI account for 89% of AI startup revenue: Even with fewer people trusting Sam Altman, his company remains a major player in the AI landscape. But they are giving up the number one spot to Anthropic. However, both companies account for a staggering 89% of all AI startup revenue. Crazy!

Andrej Karpathy joins Anthropic’s R&D team: Yes, you read that right. The co-founder of OpenAI and one of the sharpest minds in machine learning, AI research, and AGI is joining Anthropic. It seems like Dario is collecting great AI talent by the minute, like Thanos was collecting infinity stones in the Avengers universe.

BuzzFeed is still alive, but still a weird company: Jonah Peretti was, or still is, the CEO of BuzzFeed and was recently on the Decoder podcast with Nilay Patel. He elaborated on why they sold portions of the company, how the klickbait GOAT got paid by Meta, why they went bust, and how AI will save them.

And that’s a wrap for the twelfth full issue of Internet Native Capital.

The world of AI is not slowing down, and it seems like we have entered the Wall Street AI era. However, this seems to buy only time for OpenAI.

They are currently losing out to Anthropic and, I would argue, to Google as well after the search giant’s announcements this week.

Sam has to find new ways to keep engagement with OpenAI high. Let’s see if he is successful with DeployCo or potentially with an IPO.

After the win in court, nothing is holding him back from using this as a backup plan.

Whatever happens, it will be a great storyline for me to do a follow-up.

See ya!

Isn't the question here - why isn't this just another consulting program in an AI wrapper...i am sure many people who have have run businesses will tell you - the notion of inserting an FDE into business to define value added use case cases that are coherent with the overall business strategy is not trivial.

I think Altman was in the "villain phase" for a year already. This type of guys are truly disconnected from reality and I believe this is going to be another WeWork scenario.